“Kimberly-Clark is buying Kenvue” sounds cleaner than the actual deal. Kenvue holders are not getting a plain cash exit. Most of the consideration is Kimberly-Clark stock, which means the value can move before the deal closes.

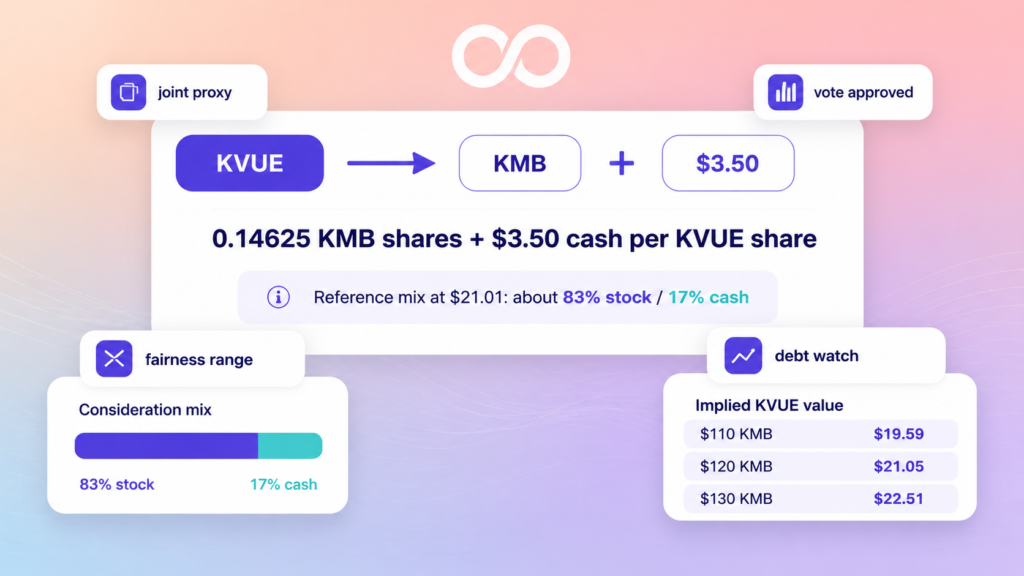

The formula in the merger documents is 0.14625 Kimberly-Clark shares plus $3.50 in cash for each Kenvue share. The joint proxy/prospectus framed that package at about $21.01 per Kenvue share using Kimberly-Clark’s October 31, 2025 closing price. Back into the formula and you get a KMB reference price of roughly $119.7.

That mix matters. About $17.51 of the $21.01 came from stock, so the reference consideration was roughly 83.3% stock and 16.7% cash. A retail holder who treats this like a fixed $21.01 takeout is reading the wrong deal.

Start with the formula, not the headline

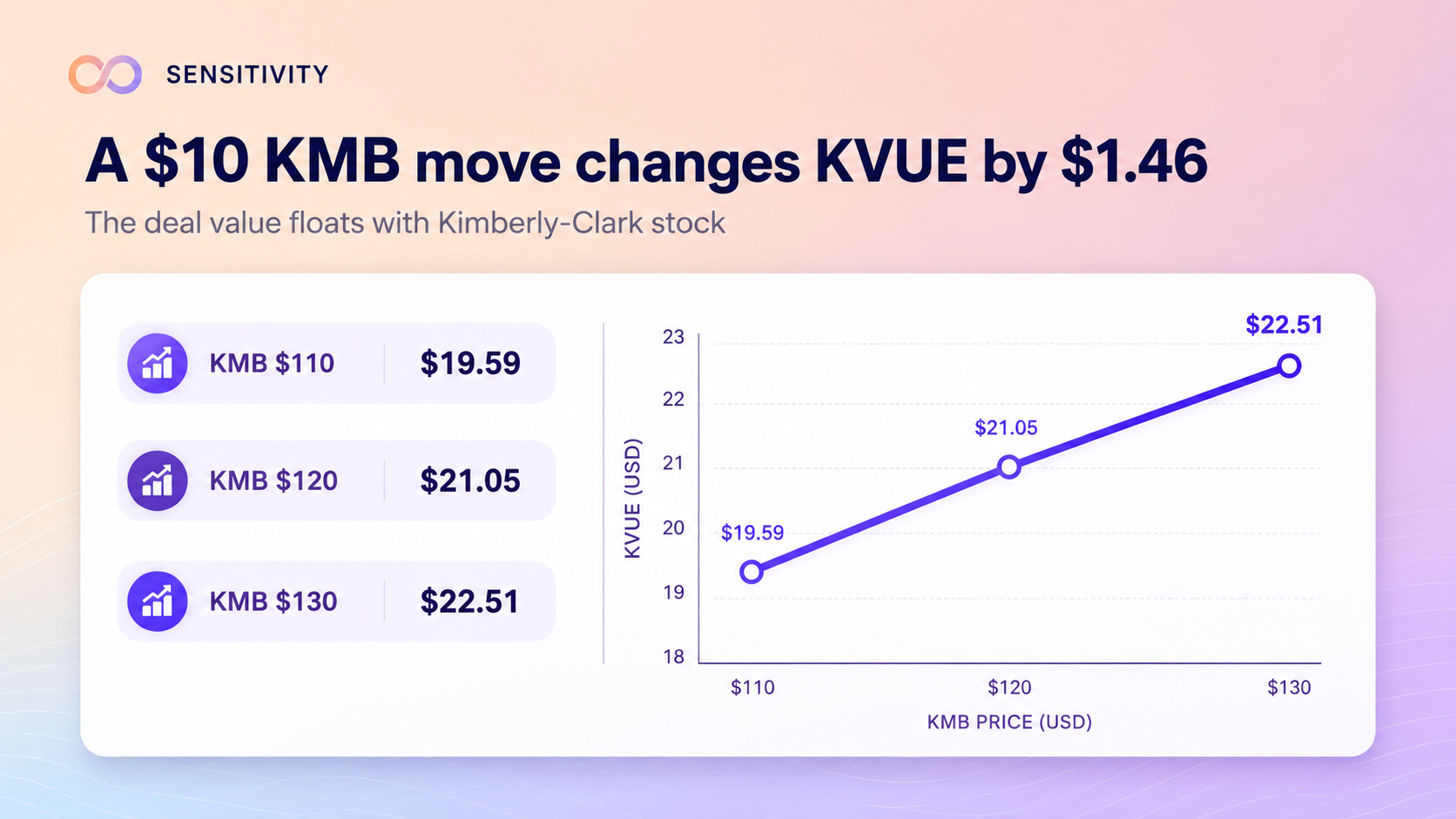

The cash piece is fixed at $3.50. The rest moves with Kimberly-Clark. Every $10 move in KMB changes the implied Kenvue consideration by about $1.46 before you even get to spread, timing, or regulatory risk.

A few quick marks show the shape of it. If KMB trades at $110, the formula gives about $19.59 per Kenvue share. At $120, it gives about $21.05. At $130, it gives about $22.51. The deal spread is sitting on top of that moving base.

So the first question is not “what was the announcement value?” It is: what is the implied Kenvue value today, using today’s KMB price?

-

Formula: 0.14625 × KMB share price + $3.50.

-

Proxy reference value: about $21.01 per KVUE share.

-

Implied KMB reference price: roughly $119.7.

-

Reference mix: about 83.3% stock, 16.7% cash.

-

A $10 move in KMB changes implied KVUE value by about $1.46.

Kenvue holders need to underwrite Kimberly-Clark

If the merger closes, legacy Kenvue holders are expected to own about 46% of the combined company. Legacy Kimberly-Clark holders are expected to own about 54%. That is not a tiny stock kicker; it is a real handoff from a standalone Kenvue thesis into a combined Kimberly-Clark / Kenvue equity story.

The scale is close enough that the deal should not be treated like a bolt-on. The proxy cited roughly $16.8B of 2024 net sales for Kimberly-Clark and roughly $15.5B for Kenvue. Simple addition puts the two at about $32.3B of 2024 sales before pro forma adjustments, roughly 52% from KMB and 48% from KVUE.

Using the same cited 2024 figures, simple combined operating profit was about $4.5B and simple combined net income was about $3.2B. This is not a forecast. It is a sanity check on what Kenvue holders are rolling into.

-

Expected ownership: about 54% legacy KMB, 46% legacy KVUE.

-

Simple combined 2024 sales: about $32.3B.

-

Simple sales split: roughly 52% KMB and 48% KVUE.

-

Simple combined 2024 operating profit: about $4.5B; net income: about $3.2B.

The buyer-side issue is debt

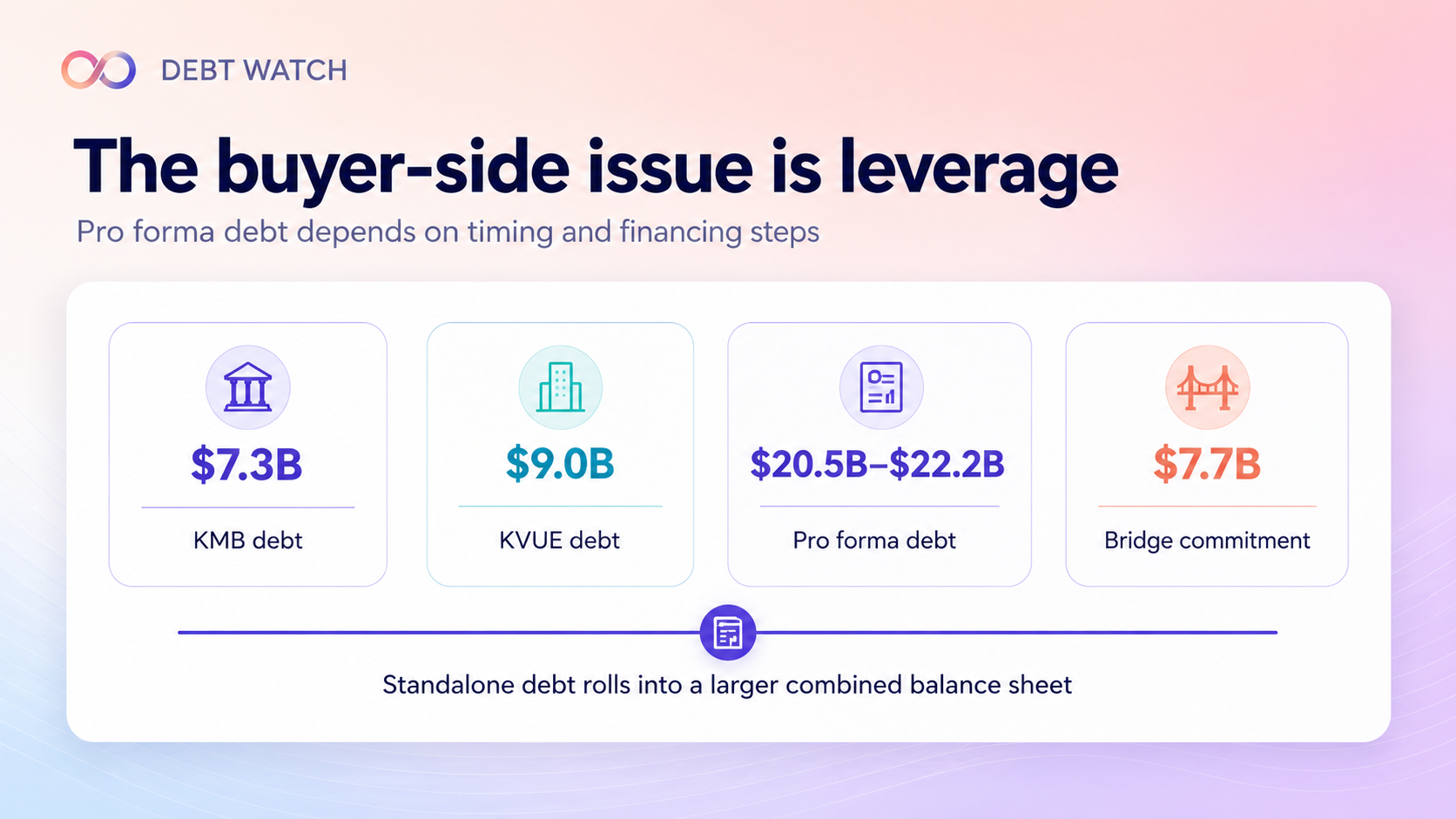

Kimberly-Clark shareholders approved the share issuance, but the balance sheet still needs attention. The proxy says Kimberly-Clark had about $7.3B of outstanding indebtedness as of September 30, 2025. Kenvue had about $9.0B as of September 28, 2025.

After giving effect to the deal mechanics in the proxy, pro forma combined debt was estimated at about $20.5B assuming the merger had closed on September 30, 2025. The same disclosure says that number could rise to $22.2B if the IFP Transaction closes after the merger closing.

Against the simple $32.3B combined 2024 sales base, those debt figures equal roughly 63.5% to 68.7% of sales. That is a rough scale marker, not a credit ratio, but it explains why financing updates deserve more than a footnote.

There is also bridge financing in the file: K-C entered into a $7.7B bridge facility commitment with JPMorgan Chase Bank on November 2, 2025, and $3.8B of those bridge commitments were terminated on December 9 after later financing steps.

-

Standalone debt: about $7.3B at KMB and $9.0B at KVUE.

-

Pro forma combined debt estimate: about $20.5B, with a possible path to $22.2B depending on IFP Transaction timing.

-

Debt compared with simple combined 2024 sales: roughly 63.5% to 68.7%.

-

Bridge commitment: $7.7B originally; $3.8B later terminated.

The vote was lopsided. The deal still has a calendar.

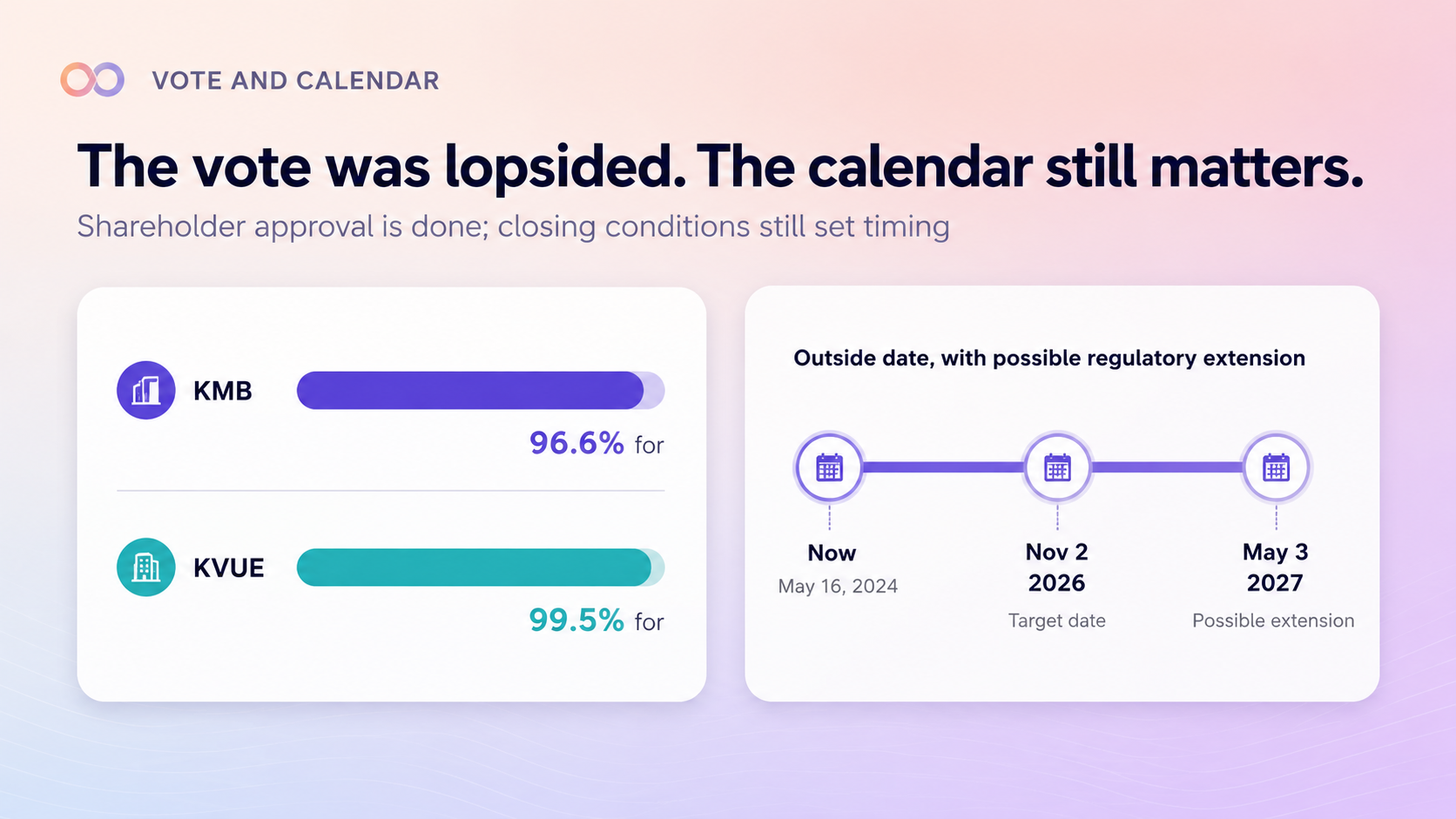

The shareholder vote is no longer the main open question. Kimberly-Clark reported 239,054,286 votes for the share issuance proposal versus 8,439,618 against. Kenvue reported 1,489,923,158 votes for the merger proposal versus 7,467,731 against.

Measured only against votes for and against, that is roughly 96.6% support at Kimberly-Clark and 99.5% support at Kenvue. Shareholder approval was not the hard part after January 2026.

The closing conditions still matter: regulatory approvals, Nasdaq listing approval for the Kimberly-Clark shares, no legal restraint, registration-statement effectiveness, representations and warranties, and covenant performance. The outside date is November 2, 2026, with an automatic extension to May 3, 2027 if the only unsatisfied conditions relate to certain regulatory approvals or legal restraints.

-

KMB vote: 239.1M for, 8.4M against.

-

KVUE vote: 1.490B for, 7.5M against.

-

Support excluding abstentions/other categories: roughly 96.6% for KMB and 99.5% for KVUE.

-

Outside date: November 2, 2026; possible extension to May 3, 2027.

Kenvue’s litigation file did not disappear

The proxy’s background section says Kenvue and Kimberly-Clark discussed scientific studies related to acetaminophen use in pregnancy, public statements from medical providers and health authorities, legal and regulatory considerations for acetaminophen and related litigation, and ongoing talc litigation matters.

That is not a damages estimate. It is not a verdict on the claims. But it does tell you the buyer spent diligence time there, which is enough reason for a retail holder to keep the legal file next to the merger file.

What could change before close? Later filings could add risk-factor language, describe new developments, or give more detail on how management views the exposure. Nothing material may change, too. The point is narrower: Kenvue’s legal backdrop remains part of the combined-company story.

-

Proxy diligence topics include acetaminophen-related and talc-related matters.

-

Do not infer a damages number from that disclosure alone.

-

Later filings may matter if they change legal-risk language, reserves, indemnity discussion, or closing-condition commentary.

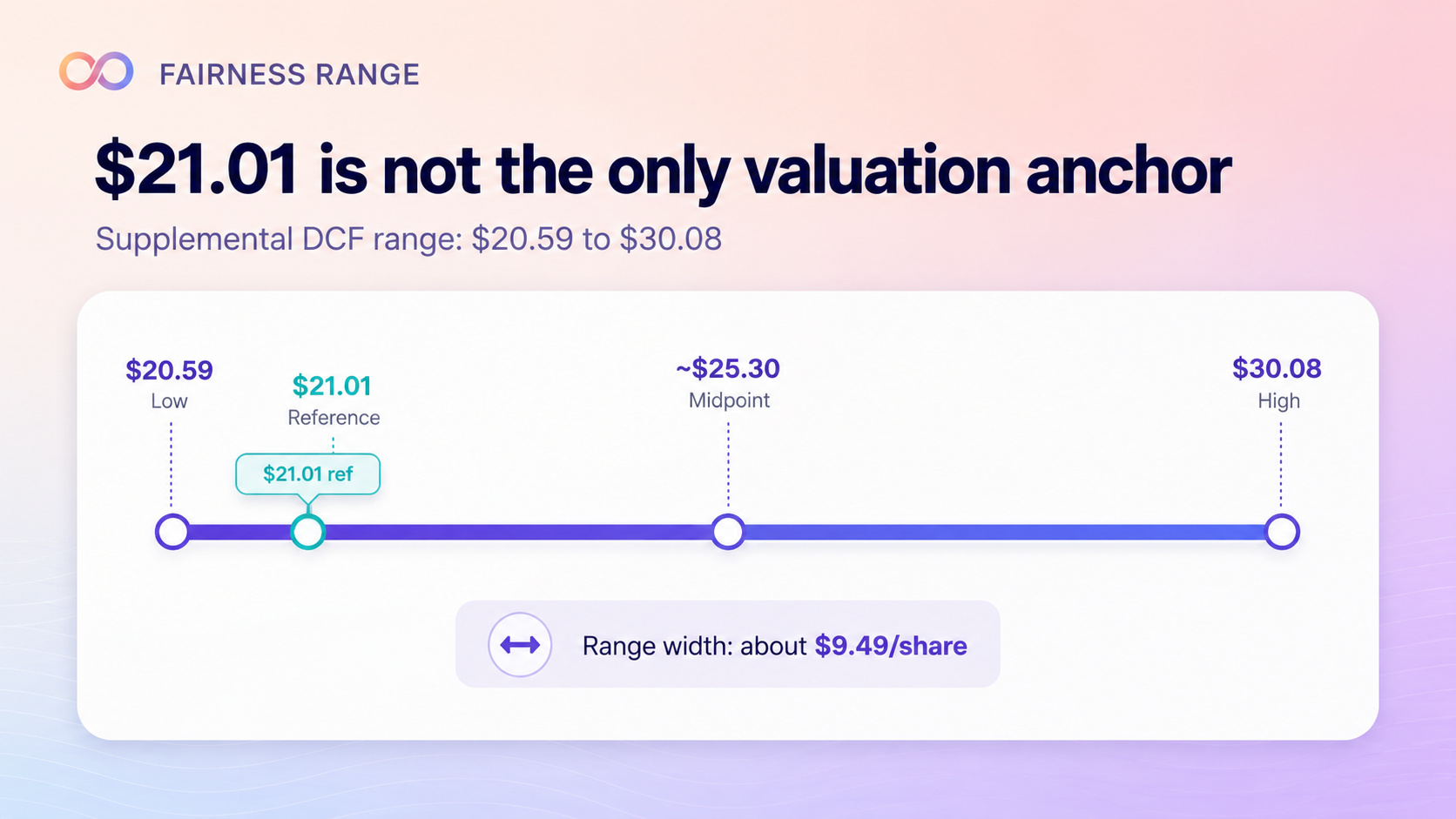

The fairness range makes $21.01 look less final

The January 16 supplemental disclosures added detail to Goldman Sachs’ financial-advisor analysis for Kenvue. The illustrative discounted cash flow analysis, using assumptions approved by Kenvue management, produced a present-value-per-share range of $20.59 to $30.08.

That is a wide range: about $9.49 from low to high, with a midpoint around $25.3. The $21.01 proxy reference value sits about 2.0% above the low end, about 17.1% below the midpoint, and about 30.2% below the high end.

That comparison does not tell you to accept or reject the deal. It tells you not to let the announcement value become the only valuation anchor. The same supplemental disclosure cited net debt and debt-like items of $7.902B as of the end of Q3 2025 and a fully diluted share count range of about 1.931B to 1.949B as of October 30, 2025. Those numbers belong in the same file as the exchange ratio, the current KMB price, the Kenvue market price, and the remaining spread.

-

Goldman Sachs DCF range cited for Kenvue: $20.59 to $30.08 per share.

-

Range width: about $9.49; midpoint: roughly $25.3.

-

Proxy reference value versus range: about 2.0% above the low end, 17.1% below the midpoint, 30.2% below the high end.

-

Other supplemental inputs: $7.902B of net debt and debt-like items; about 1.931B to 1.949B fully diluted shares.

What can still move the trade

For Kenvue holders, the first moving part is obvious: Kimberly-Clark’s stock price. The second is time. A small spread can look fine on a short closing window and less interesting if the regulatory calendar drags toward the outside date.

For Kimberly-Clark holders, the next debt update may matter more than the next deal headline. Watch debt issuance, bridge takedowns, rating-agency language, and management’s comments on dividends, buybacks, integration spending, and debt paydown.

Then there is the legal file. If later filings change Kenvue’s risk language around acetaminophen or talc matters, the market may change how it values the stock component, the standalone fallback, or the combined-company equity.

The cleanest investor checklist is short: recalc implied KVUE value, compare it with the market price, check which closing conditions remain open, read any financing update, and decide whether you actually want to own Kimberly-Clark after close.

-

Current implied KVUE value using KMB’s latest price.

-

Spread versus KVUE’s market price.

-

Open closing conditions and regulatory timing.

-

Debt financing, bridge, rating, dividend, and buyback language.

-

Any later filing that changes the litigation or risk-factor picture.

-

Your own answer to the post-close question: would you hold the combined company?

Vynt is in public beta for investors who want the filing trail next to the thesis. Use it to track the Kimberly-Clark / Kenvue deal terms, implied value, vote results, closing conditions, debt disclosures, and later filings without losing the source text.

Leave a Reply